TACTICAL STRATEGIES

PREMIER WEALTH TACTICAL & PREMIER WEALTH TACTICAL CORE

Despite concerns over inflation and earnings declines, stocks have been hanging tough. Markets rose a little over one percent in April. Are investors being too complacent or will the economy pull off the difficult soft landing in the face of tightening financial conditions?

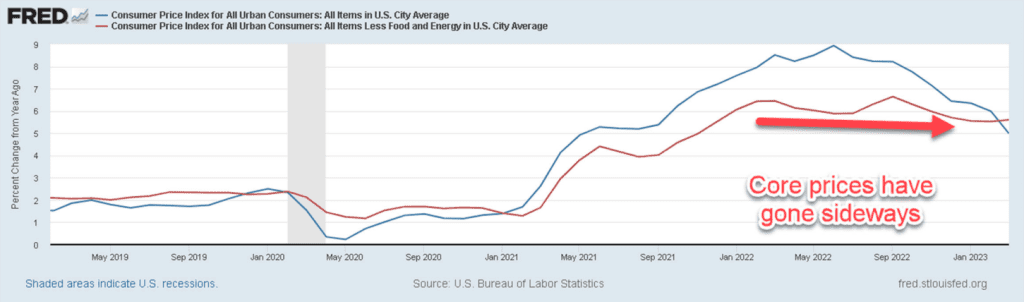

Inflation has been the chief concern for the economy. The good news is that inflation is clearly coming down from its high levels. However, core prices – the Fed’s preferred measure of inflation which excludes food and energy – has been stickier than hoped. This likely means the Fed Funds rate will remain higher for longer.

Meanwhile, corporate earnings are muted but maybe not as bad as initially feared. With 53% of the S&P 500 having already reported, 79% have beaten their earnings estimates while 74% have topped revenue targets. True, most of that is a function of lowered expectations, but some large-cap tech bellwethers delivered robust reports. Tech titans Microsoft, Alphabet, Meta, and Amazon powered through earnings, easily beating their targets. Apple will also be reporting this week- their results will surely be closely watched.

As a result, stock returns have been narrowly focused year to date. Large-cap Tech has carried the market with eight Mega cap stocks making up 6.44% of the 7.65% gain in the S&P 500 year to date. The other 492 stocks in the S&P 500, in aggregate, have gained a mere 1.21% this year.

On the economic front, the Fed recently raised rates 25bps and signaled that a pause could be at hand but that would depend on incoming data. Chairman Powell did also reiterate that the Fed does not see the conditions for rate cuts this year based on their current forecast. That is at odds with what the market has been pricing and could be a point of contention for markets. Higher rates have clearly put more pressure on the regional banks as depositors continue to move money out. The regional banks index made fresh lows this week. The likely reason is the rate differential between what these banks are paying their depositors and what they can get in money markets. On average they are paying half a percent when money market funds are yielding 4.5%.

Another potential market-moving economic release is Friday’s jobs report. A strong jobs number would affirm the Fed’s recent mantra of higher for longer in terms of rates while a weaker number would boost the case for a pivot happening sooner.

On a technical basis, the market highs seen back in February have acted as some resistance on the upside. A breakout above those levels would be a positive development.

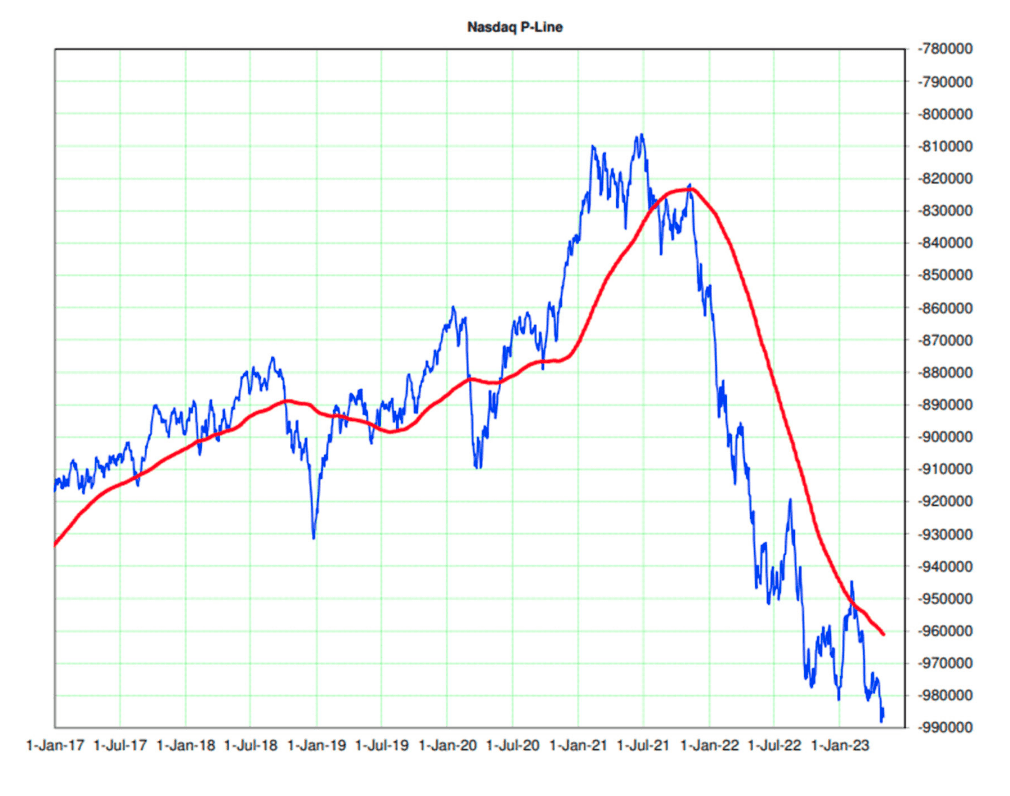

An area of concern is the top-heavy nature of the market mentioned above. Consider the breadth in the Nasdaq. The cumulative advance-decline line is currently sitting around the lows for this cycle. Markets are deemed to be much healthier when the vast majority of issues are participating.

While we have seen plenty of volatility over the last year, it is surprising to many that the S&P 500 trades around the same levels it was at this time in 2022. The indices have essentially traded sideways between 3600 and 4200. Hopefully, the long trading range turns out to be a classic bottoming process that historically follows a bear market before a recovery – unlike the V-shaped recoveries seen in recent years.

Whether it will ultimately be defined as a bottoming process will only be known in retrospect. However, for now, the back-and-forth action certainly gives hope for one. With the rest of earnings season rolling out in the next couple of weeks, including the behemoth in Apple, the market still faces some tests ahead.

TACTICAL OPPORTUNITY

Old school Tech stocks have been doing better than most as Microsoft, Apple, and Google are holding up well so far. Good earnings from Microsoft and Google have played a role in that. Apple’s earnings are on deck and could bolster the status quo if they can do the same. Until the market can establish an up or down trend with consistency, our percent invested will likely remain largely the same.

FULLY INVESTED STRATEGIES

ETF SECTOR ROTATION

Clear sector leadership remains elusive in 2023. Different sectors have taken the lead only to give it back shortly after. Energy has been lagging as of late with the price of oil having taken a hit. Outperforming over that past month have been Communications and Consumer Staples. We are overweight Tech, Healthcare, and Energy, with the latter getting a close look in the face of some recent weakness. It is not unusual for Energy to be a volatile trade. Despite bank headlines, the Financial sector has held up ok outside of regional banks.

The narrow market has been tough to beat, with the majority of sectors lagging. For broad markets, Growth and Value have been about the same over the last month. Small caps have hit some trouble and is behind the lagging market breadth numbers. Internationally, we are fully in on Europe and halfway on Emerging Markets.

EQUITY GROWTH OPPORTUNITY

The portfolio remained calm in April as we are on the lookout for leadership to emerge before making any major allocation changes. The tides have swayed from Growth/Technology to Value and now back to Mega-cap Technology with some strong earnings reports last week. The market is on the edge of resistance with the potential to break out of a year-long trading range. Should we get some upside momentum, we may look to increase the beta in the portfolio.

EQUITY GROWTH AND VALUE

Stocks are bumping around since the start of April with both winners and losers showing no real direction. Some energy and industrial names are paring back like Valero Energy and Carrier Global. On the other side, we had good months from names like Chipotle, Molson Coors, and Vertex Pharma. We will continue to look for some rotation opportunities as the market continues to look for its footing.

EQUITY DIVIDEND INCOME

Dividend paying stocks have been treading water in the face of some tough trading recently. Energy holdings have contributed to that as they are giving back some past gains. We have pared some holdings there. Consumer staple stocks had positive moves in recent weeks. No significant changes are expected.

RISK BLENDED STRATEGIES

Our Risk Blended Strategies are a combination of both Premier Wealth Tactical Core and ETF Sector Rotation. Please see the above commentary for more information on each strategy.

- Churchill Moderate: 70% Premier Wealth Tactical Core / 30% ETF Sector Rotation

- Churchill Moderately Aggressive: 50% Premier Wealth Tactical Core / 50% ETF Sector Rotation

- Churchill Aggressive: 30% Premier Wealth Tactical Core / 70% ETF Sector Rotation

Best regards,

CHURCHILL MANAGEMENT GROUP

877-937-7110

[email protected]

** This report is meant to inform the reader of our current market opinion, which we, as professional money managers, use in our decision-making. It should be noted that stock market and bond market data are subject to varying interpretations and any one interpretation will not necessarily guarantee investment success. The information obtained from the sources specified herein and used as a basis for our current market opinion is believed reliable, but we do not guarantee the accuracy of such information. The references to specific investments were chosen based on our current market outlook, as examples representing how aspects of the market have performed and as representation of what a strategy might own. Those are included for informational purposes only and past specific investment advice does not guarantee future results.